Understanding Methods and Assumptions of Depreciation.

Understanding Methods and Assumptions of Depreciation. greenwood lake, ny deaths

The corporation first multiplies the basis ($1,000) by 40% (the declining balance rate) to get the depreciation for a full tax year of $400. The midpoint of each quarter is either the first day or the midpoint of a month. The General ledger For additional guidance, see Notice 2008-25 on page 484 of Internal Revenue Bulletin 2008-9, available at, If, in any year after the year you claim the special depreciation allowance for qualified Recovery Assistance property, the property ceases to be used in the Kansas disaster area, you may have to recapture as ordinary income the excess benefit you received from claiming the special depreciation allowance.

You reduce the adjusted basis ($173) by the depreciation claimed in the fifth year ($115) to get the reduced adjusted basis of $58.

The furniture is also 7-year property, so you use the same 200% DB rate of 0.28571. Silver Leaf, a retail bakery, traded in two ovens having a total adjusted basis of $680, for a new oven costing $1,320. Stock possessing more than 5% of the total combined voting power of all stock in the corporation. And estimate made by the company of the dollar amount that can be recovered for the asset at the end of its useful life when it is disposed of or sold/traded. After you figure the full-year depreciation amount, figure the deductible part using the convention that applies to the property. To qualify for the section 179 deduction, your property must have been acquired by purchase. Instead, it sells them through wholesalers or by similar arrangements in which a dealer's profit is not intended or considered. It also discusses other information you need to know before you can figure depreciation under MACRS. An individual is considered to own the stock or partnership interest directly or indirectly owned by or for the individual's family. See Carryover of disallowed deduction, earlier. Finally, it explains when and how to recapture MACRS depreciation. In addition, due to the nature of utility plant and power generation assets, the group and composite methods of depreciation are commonly applied in depreciating multiple assets or asset groups. This includes listed property used 50% or less in a qualified business use. For each GAA, record the depreciation allowance in a separate depreciation reserve account. The Volunteer Income Tax Assistance (VITA) program offers free tax help to people with low-to-moderate incomes, persons with disabilities, and limited-English-speaking taxpayers who need help preparing their own tax returns.

This method will produce results that vary annually depending on the number of units made. The Social Security Administration (SSA) offers online service at SSA.gov/employer for fast, free, and secure online W-2 filing options to CPAs, accountants, enrolled agents, and individuals who process Form W-2, Wage and Tax Statement, and Form W-2c, Corrected Wage and Tax Statement. Determine the depreciation rate for the year. TAS can provide a variety of information for tax professionals, including tax law updates and guidance, TAS programs, and ways to let TAS know about systemic problems youve seen in your practice.

Treat the carryover basis and excess basis, if any, for the acquired property as if placed in service the later of the date you acquired it or the time of the disposition of the exchanged or involuntarily converted property. The recipient of the property (the person to whom it is transferred) must include your (the transferor's) adjusted basis in the property in a GAA. Understanding Methods and Assumptions of Depreciation.

However, original use does not include the cost of reconditioned or rebuilt property you acquired.

You are a paper manufacturer. The price that property brings when it is offered for sale by one who is willing but not obligated to sell, and is bought by one who is willing or desires to buy but is not compelled to do so. Even if you are not using the property, it is in service when it is ready and available for its specific use.

Then, determine the depreciation for the short tax year. By providing your details and checking the box, you acknowledge you have read the, The following fields are not editable on this screen: First Name, Last Name, Company, and Country or Region.

You must generally file Form 3115, Application for Change in Accounting Method, to request a change in your method of accounting for depreciation. Step 8Using $20,000 (from Step 7) as taxable income, XYZ's actual charitable contribution (limited to 10% of taxable income) is $2,000. Summary: This table is used to determine the percentage rate used in calculating the depreciation of property.

The FMV of the property is the value on the first day of the lease term.

If you dispose of the property before the end of the recovery period, figure your depreciation deduction for the year of the disposition the same way.

The corporation first multiplies the basis ($1,000) by 40% to get the depreciation for a full tax year of $400. "Publication 946 How to Depreciate Property," Pages 9, 40, 46, and 109. Any race horse over 2 years old when placed in service. The amount realized also includes any liabilities assumed by the buyer and any liabilities to which the property transferred is subject, such as real estate taxes or a mortgage. After the due date of your returns, you and your spouse file a joint return.

This rule applies to any 4-wheeled vehicle primarily designed or used to carry passengers over public streets, roads, or highways that is rated at more than 6,000 pounds gross vehicle weight and not more than 14,000 pounds gross vehicle weight. Summary: This table lists the recovery periods (in years) for depreciable assets used listed business activities. Any transaction between members of the same affiliated group during any year for which the group makes a consolidated return.

You must stop using the tables if you adjust the basis of the property for any reason other than: An addition or improvement to that property that is depreciated as a separate item of property. This is also true for a business meeting held in a car while commuting to work.

It results in fewer errors, is the most consistent method, and transitions well from company-prepared statements to tax returns. You figure this by subtracting the first year's depreciation ($107) from the basis of the furniture ($1,000). This chapter defines listed property and explains the special rules and depreciation deduction limits that apply, including the special inclusion amount rule for leased property. The double declining balance method of depreciation, also known as the 200% declining balance method of depreciation, is a form of accelerated depreciation. A capitalized amount is not deductible as a current expense and must be included in the basis of property.

A corporation's taxable income from its active conduct of any trade or business is its taxable income figured with the following changes. in chapter 4.

To figure your depreciation deduction under MACRS, you first determine the depreciation system, property class, placed in service date, basis amount, recovery period, convention, and depreciation method that apply to your property. Depreciating an asset over a life that is less than its properly estimated probable service life results in excessive charges to operations and fully depreciated assets that are still in use, both of which are inconsistent with the conceptual purpose of More than 10% of the value of the outstanding stock of the corporation. The one who acts on behalf of another as a guardian, trustee, executor, administrator, receiver, or conservator.

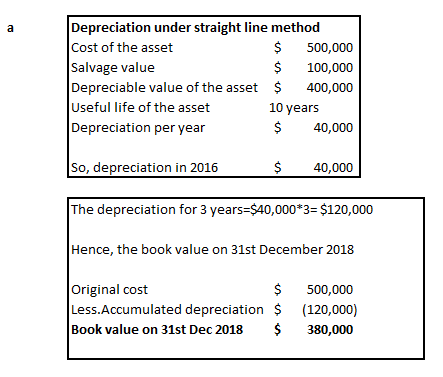

You figure depreciation for the year you place property in service as follows. Tax Planning and Compliance. Depreciation using the straight-line method reflects the consumption of the asset over time and is calculated by subtracting the salvage value from the asset's purchase price.

To figure your MACRS depreciation deduction for the short tax year, you must first determine the depreciation for a full tax year.

Once you start using the percentage tables for any item of property, you must generally continue to use them for the entire recovery period of the property.

Accounting also allows companies to comply with tax laws and regulatory requirements. The table lists the asset class, description of asset, the recovery periods for: Class Life (in years), General Depreciation System (Modified Accelerated Cost Recovery System) and Alternative Depreciation System. The result is 40%.

Use Form 4562 to figure your deduction for depreciation and amortization. However, if MACRS would otherwise apply, you can use it to depreciate the part of the property's basis that exceeds the carried-over basis. Property converted from personal use to business use in the same or later tax year may be qualified property. For a discussion of when property is placed in service, see When Does Depreciation Begin and End, earlier. Divide the number of your shares of stock by the total number of outstanding shares, including any shares held by the corporation. This GAA is depreciated under the 200% declining balance method with a 5-year recovery period and a half-year convention.

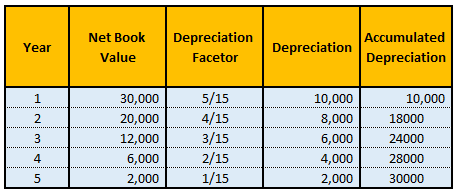

Figuring depreciation under the declining balance method and switching to the straight line method is illustrated in Example 1, later, under Examples. The basis of an item of property for purposes of figuring gain on a sale without taking into account any depreciation taken in earlier years but with adjustments for other amounts, including amortization, the section 179 deduction, any special depreciation allowance, any deduction claimed for clean-fuel vehicles or clean-fuel vehicle refueling property placed in service before January 1, 2006, and any electric vehicle credit.

Consider removing one of your current favorites in order to to add a new one.

To figure depreciation on passenger automobiles in a GAA, apply the deduction limits discussed in chapter 5 under Do the Passenger Automobile Limits Apply. It lists the percentages for property based on the Straight Line method of depreciation using the Mid-Quarter Convention and Placed in Service in Second Quarter.

It lists the percentages for property based on the 150% Declining Balance method of depreciation using the Mid-Quarter Convention, Placed in Service in Second Quarter. It improve the transparency of financial reporting in all countries. The applicable convention (discussed earlier under Which Convention Applies) affects how you figure your depreciation deduction for the year you place your property in service and for the year you dispose of it. The IRSs commitment to LEP taxpayers is part of a multi-year timeline that is scheduled to begin providing translations in 2023. Property contained in or attached to a building (other than structural components), such as refrigerators, grocery store counters, office equipment, printing presses, testing equipment, and signs.

It lists the percentages for property based on the Straight Line method of depreciation using the Mid-Quarter Convention and Placed in Service in First Quarter. Answer: Applied to a group of homogeneous assets.

To determine the midpoint of a quarter for a short tax year of other than 4 or 8 full calendar months, complete the following steps. Passenger automobiles (as defined later).